How is a business sold?

When buying a business of any nature and size, the fundamental sale process is the same:

How is the sale of a business structured?

There are 2 main approaches to selling a typical business:

What are the differences between an asset sale and a share sale?

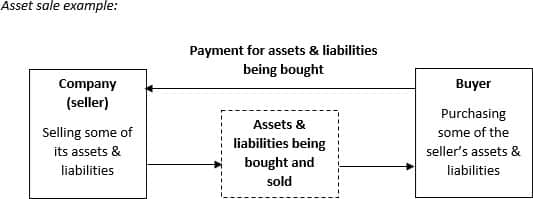

With an asset sale, a seller will only sell specific assets and liabilities which they agree with the buyer. This enables the seller to select only those aspects of the business that they want to sell. It also enables a buyer to exclude any liabilities that they don’t want to take over, and leave those with the seller.

After completion of the asset sale:

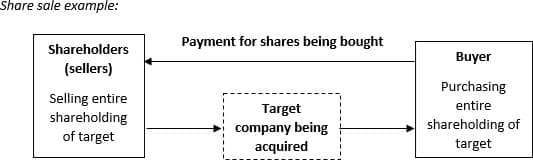

With a share sale, the seller will sell the target company “warts and all”. The buyer will purchase the entire shareholding of the company and therefore acquires all of its assets and all of its liabilities.

After completion of the share sale:

How to choose between an asset sale and a share sale:

The circumstances of the business sale, and advice from professional advisers particularly surrounding tax issues, will usually dictate whether the sale of a business should be structured as an asset sale or a share sale. We would always advise prospective buyers and sellers of a business to take tax advice early on in the sale negotiations.

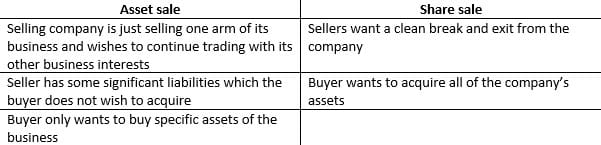

As a general starting point, here are some typical situations which would lean towards an asset sale and share sale:

Generally an asset sale is viewed as more buyer-friendly, and a share sale is viewed as more seller-friendly. The final decision on structure is likely to be determined by the negotiation power of both parties, and the tax advice received.

What happens to the employees of the business being sold?

With a share purchase, the employees remain within the same target company.

With an asset purchase, there are special rules (known as “TUPE”) which determine whether or not the employees will automatically transfer to the buyer, or whether they will remain with the selling company.

What are the key negotiation points when selling a business?

Every business and transaction is unique, so there is no one-size-fits-all approach when it comes to negotiating the terms of a business purchase. However, there are some key points which will apply to every business sale, and some additional points which prospective sellers should consider including:

Some negotiation points might be revealed as a result of the due diligence process.

Agreeing heads of terms for the sale of a business

Heads of terms are a very useful tool when selling a business. They enable a buyer and a seller to set down what terms they have agreed for the sale and purchase of the business. This means that any key issues can be agreed and any potential problems are managed at an early stage of the sale process, before incurring any significant legal costs. See our guide on heads of terms for more information.

Agreeing the other key agreements and documents

The main asset sale agreement or share sale agreement will contain various provisions relating to the sale of the business. These agreements are extremely important in the purchase of a business, and must be negotiated carefully.

Yes, you will likely need a solicitor to sell your small business. A solicitor ensures that the legal aspects of the sale are handled correctly, including drafting and reviewing the sale agreement, conducting due diligence, and ensuring compliance with relevant laws. They play a critical role in protecting your interests, managing risks, and ensuring the transaction is legally valid. Without a solicitor, you risk overlooking important legal requirements or liabilities, which could lead to costly disputes in the future.

Key reasons to use a solicitor:

Working with a solicitor ensures that the sale of your business is legally sound and helps you achieve a successful and stress-free transaction.

If you need any advice on selling a business, please contact a member of our corporate and commercial law team in confidence here or on 02920 829 100 for a free initial call to see how they can help.

To speak to one of our experts today, please contact us on 02920 829 100 or by using our Contact Us form for a free initial chat to see how we can help.

Notifications