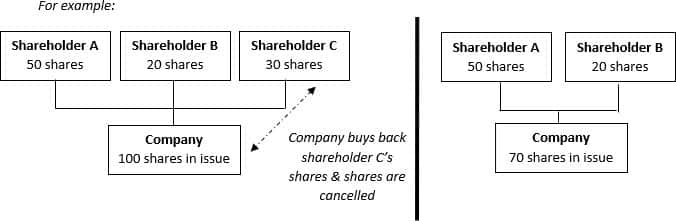

What is a company share buy back?

A company share buy back is exactly that – the company buying its own shares back from one or more of its shareholders. The shares are then either cancelled (so they no longer exist), or are held by the company in treasury.

When would a company want to buy its own shares?

There are a number of reasons why a company share buy back can be a useful tool. These include:

Many of these decisions will be driven by tax advice from the company’s accountant.

Are there restrictions on when a company can buy its own shares?

The ability of a company to buy back its own shares is carefully controlled by the Companies Act. A buy back can only validly occur provided the company follows the procedure set down by law. This includes:

In addition, the company’s own articles of association may restrict its ability to buy back its own shares and these must be checked in all cases.

How does a share buy back work?

The procedure for a share buy back varies depending on whether they company is buying back its shares out of available profits, or out of capital. The procedure for purchasing out of available profits is much quicker and simpler, as the company has enough cash to fund the buyback. Where a buyback is to be funded out of the company’s capital reserves, additional steps must be taken including publishing a public notice of the intention to use the capital reserves. Any creditors of the company then has an opportunity to object to the proposed purchase

There are some exceptions where, for example, the buy back is pursuant to an employee share scheme.

In all cases the company will need to have a proper share buy back agreement in place between itself and the selling shareholder(s).

What happens if the share buy back procedure is not followed?

If the correct procedure is not followed then the share buy back will be void. There are various steps which can be taken to potentially ratify the buy back, however the best course of action is to take proper advice at the outset to ensure that the buy back documents are correctly drawn up.

If you need any advice on company share buy backs, please contact a member of our corporate and commercial law team in confidence here or on 02920 829 100 for a free initial call to see how they can help.

To speak to one of our experts today, please contact us on 02920 829 100 or by using our Contact Us form for a free initial chat to see how we can help.